Session VIII - General Interest

Sat., 10/12/13 Topics of General Interest, PAPER #88, 12:42 pm OTA 2013

Does Fracture Care Make Money for the Hospital? An Analysis of Hospital Revenue and Cost for Treatment of Common Fractures

Conor Kleweno, MD; Robert O’Toole, MD; Jeromie Ballreich, MHS; Andrew Pollak, MD;

R Adams Cowley Shock Trauma Center, Department of Orthopaedic Surgery,

University of Maryland School of Medicine, Baltimore Maryland, USA

Purpose: With increasing health-care costs and decreasing revenue, understanding the profitability of orthopaedic trauma care is becoming progressively more important. The relative profitability of caring for patients with various fractures is unknown, however. The purpose of this study was to determine the relative profitability to the hospital for a selection of specific common fractures.

Methods: Data were collected from hospital medical and financial records at a single large academic urban trauma center with a state-regulated hospital reimbursement system. This state’s unique legislatively mandated system ensures that the burden of uncompensated care to the hospital is addressed and that cost-shifting from the uninsured to the insured patients is normalized across all payers. Hospital medical and financial records of 1020 patients admitted from 2008 to 2012 with a principal diagnosis of an acute traumatic fracture requiring surgical treatment were reviewed. Patients whose principal diagnosis fit into 1 of 5 common anatomic categories based on their ICD-9-CM codes were included. 275 acetabular fractures, 65 pelvis fractures, 277 hip fractures, 255 femoral shaft fractures, and 148 tibia shaft fractures were identified. Patients that sustained one of these fractures but had a different principal diagnosis were excluded. The net revenue, total cost of inpatient care (direct variable expense plus direct fixed expense), and direct margin (net revenue minus total cost, ie, profit) for each patient’s acute inpatient hospital course were collected. Margins were compared using a one-way analysis of variance.

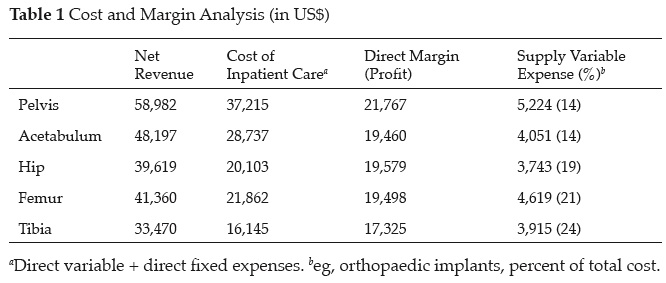

Results: The overall mean direct margin (profitability) of the cohort was $19,526 per patient. The overall mean revenue was $44,326 per patient and the overall mean cost of inpatient care was $24,812 per patient ($16,526 mean direct variable expense and $8,286 mean direct fixed expense). Factors most influencing cost included of length of stay ($6403, 26%) and operating room use ($6354, 26%). In addition, the supply variable expense (eg, orthopaedic implants) averaged $4169 (17% of total cost). Of 1020 patients, only 44 (4%) had a negative direct margin (indicating a net loss to the hospital). The most profitable diagnosis was pelvis fracture (P <0.05). Table 1 demonstrates cost and margin analysis for each fracture.

Conclusions: This rate-regulated system allows analysis of hospital profitability in the context of a normalized revenue stream that should approximate the overall fiscal realities of other states. Our data show that providing orthopaedic trauma care can be economically feasible and even profitable to a hospital. Understanding the relative costs and margins will help providers and hospitals target cost containment projects.

Alphabetical Disclosure Listing

• The FDA has not cleared this drug and/or medical device for the use described in this presentation (i.e., the drug or medical device is being discussed for an “off label” use). ◆FDA information not available at time of printing. Δ OTA Grant.